How the New 401(k) Executive Order Could Change Your Plan: Are You Ready for Private Equity and Crypto?

On August 7, 2025, the White House issued an executive order directing agencies to expand access to alternative assets in defined contribution (“DC”) plans. It instructs the Department of Labor (“DOL”) to reexamine and clarify ERISA fiduciary guidance on offering alternative assets (such as private placements and crypto currency) inside multi-asset funds, to consider proposing rules and guidance that may include carefully calibrated safe harbors, and to coordinate with the SEC. The order also asks the SEC to consider adjustments to accredited investor and qualified purchaser standards that could affect plan access.

Separately, the DOL has already rescinded its 2022 crypto caution. Compliance Assistance Release 2025-01 withdrew the prior warning and restored a neutral stance toward particular investment types. On August 12, 2025, the DOL also announced rescission of its December 21, 2021 supplemental statement that discouraged private equity in DC menus.

The Hidden Complexities Plan Sponsors Must Consider

Liquidity Constraints Create Real Problems

Private equity positions are illiquid and often involve multi-year lockups. That clashes with daily liquidity expectations in 401(k)s and complicates distributions, QDROs, and terminated participant withdrawals. Recent coverage highlights the challenge of redemption timing and valuation lags for private assets in DC plans.

Fee Structures Can Surprise Participants

Alternative assets typically carry higher fees than core index funds.

- Private equity funds commonly use management and performance fees, for example a “2 and 20” structure. Actual levels vary by strategy and fund.

- Equity mutual funds held by retail investors averaged about 0.40% in 2024 industrywide, and average equity mutual fund fees paid by 401(k) participants were closer to 0.26%.

- Spot Bitcoin ETF fees generally range from roughly 0.19% at the low end to about 1.5% for higher-cost products. Menu choice matters.

Higher costs do not automatically disqualify an option, but fiduciaries must document why any added expense is prudent relative to expected benefit.

Operational Burden on HR and Benefits Teams

Recordkeepers and administrators must handle complex valuation, liquidity, reconciliation, and participant communications for illiquid assets. Industry analysts expect adoption to be gradual despite policy shifts, given operational and litigation risks.

Why Sophisticated Investors Are Still Cautious

Research from the Center for Retirement Research suggests that alternatives did not boost overall public pension returns over 2001 to 2022, though they may have reduced volatility. That mixed record and significant dispersion across managers explains caution even among institutions.

For crypto, several central bank and policy studies note that unbacked crypto assets lack intrinsic cash flows and carry elevated volatility, which makes them a poor fit for unsophisticated investors and for objectives that rely on predictable funding.

Fiduciary Risk Will Not Disappear

The executive order cannot eliminate ERISA lawsuits. It may lead to guidance and safe harbors, but litigation risk remains. The Intel v. Sulyma litigation over alternative allocations in plan defaults shows how disputes can run for years across multiple courts, regardless of disclosure volume. Experts also caution that an order cannot override ERISA’s duty of prudence.

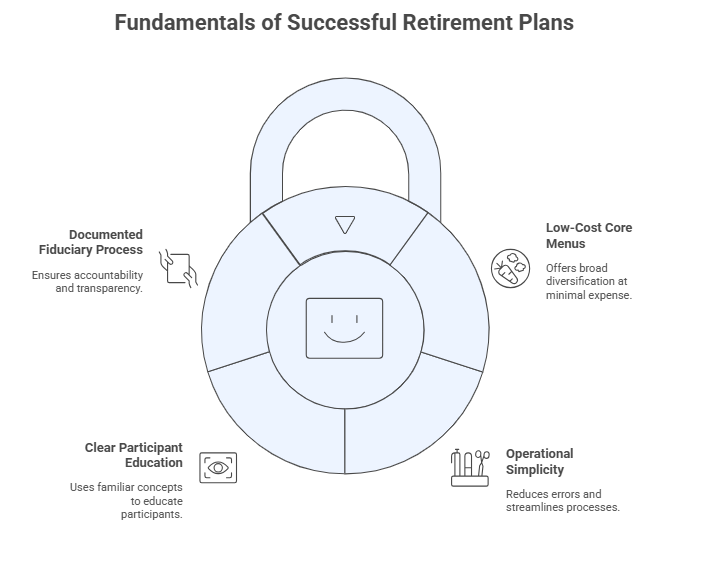

A Better Approach: Focus on Proven Fundamentals

Most successful small- and mid-sized employer plans emphasize:

- Low-cost core menus that deliver broad diversification

- Operational simplicity that reduces error risk

- Clear participant education using familiar concepts

- A documented fiduciary process that survives scrutiny

Key Questions for Plan Sponsors

- Do participants actually understand the current lineup and how to use it?

- Are plan costs at or below peer benchmarks?

- Can your HR and recordkeeper handle illiquidity, valuations, and complex communications?

- Are you prepared to justify the prudence of higher fees and reduced liquidity?

- Are savings and default rates doing the heavy lifting already?

TL; DR

The order opens a policy door, not a mandate to add alternatives. Given liquidity constraints, higher fees, administrative complexity, and legal exposure, alternative assets will be unsuitable for many employer-sponsored plans. Get the basics right first: competitive fees, strong default design, and clean administration. Revisit alternatives only if you can show a clear, participant-focused benefit and a rock-solid process.

Thank you for reading. Please review our disclosures.

Subscribe to our Newsletter and Receive Important News & Updates.

Foundation Wealth & Tax Advisors is a Fee-Only, Fiduciary, Independent Financial Advisory Firm.

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.