April 2026 Letter

As tax season finally winds down, I’m reflecting on the last several weeks working on tax returns for many of you, while simultaneously keeping a close eye on the markets.

Sitting at my desk for much of the day gives me plenty of time to listen to my favorite thought-leaders and, of course, the usual lineup on CNBC, Bloomberg, and Fox Business. It feels good to finally sit down and organize some of those thoughts into writing.

As we settle into the second quarter of 2026, markets have once again shown their flair for drama. The first three months of the year delivered more than the usual share of volatility, with several sharp pullbacks driven largely by geopolitical developments (most notably the escalation of conflict with Iran) layered on top of ongoing fiscal deficits and uncertainty around the wave of Treasury debt maturing this year (more than $10 trillion, as we highlighted in our January letter). Stocks and bonds have been trading at a noticeably wider range, and swings have been sharp enough to remind everyone that patience remains the most important investment virtue.

Recycled quotes I've used before but continue to hold true:

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

“The big money is not in the buying and selling, but in the waiting.” — Charlie Munger

Q1 Recap: A Quarter Where Diversification Earned Its Keep

What stood out during the first quarter was a meaningful rotation in market leadership. While the S&P 500 finished the first quarter down roughly 4.4%, small-cap stocks actually posted a modest gain, value-oriented companies outperformed growth names, and many international developed and emerging markets held up better than the headline U.S. index. Mega-cap technology and AI leaders noticeably lagged. Episodes like this are exactly why we maintain a global allocation and a disciplined tilt toward value and smaller companies. Diversification is not just a buzzword; it is what keeps a portfolio moving forward when market leadership changes.

This environment is also exactly why we have always placed such emphasis on liquidity management in your portfolios. For those in or approaching retirement, we continue to maintain a dedicated sleeve of short-term bonds and cash equivalents sized to cover several years of planned distributions. The goal is straightforward: give us the flexibility to ride out periods of market stress without being forced to sell risk assets at unfavorable prices. The Federal Reserve has held the federal funds rate steady at 3.50%–3.75% so far this year, and expectations for rate cuts have been pushed back significantly. In this higher-for-longer rate environment, with heavy debt maturities ahead, that liquidity bucket becomes even more valuable. As I have noted in past letters, the greatest risk investors face is rarely the volatility itself but our reaction to it. By keeping the right amount of dry powder on hand, we stay disciplined and focused on the long-term plan rather than the daily headlines.

If you are in retirement or close to retirement, expect to discuss this more in our upcoming meetings.

Private Credit: Impressive Returns, But Why We Remain Cautious

One asset class our investment strategists have helped us track for several years is the private credit market. Before going further, a quick definition is in order: private credit primarily refers to loans made by non-bank investors to privately held, middle-market companies. The largest segment is direct lending (senior loans negotiated one-on-one with the borrower and held rather than traded), but the category also includes a bunch of other subclasses like mezzanine debt, distressed debt, asset-based lending, and other specialty strategies. What ties them together is that the loans do not trade on public exchanges, which is both the source of their return premium and the source of liquidity risk.

For some of you, we have discussed small allocations on the bond side of your portfolio, but never actually pulled the trigger. The return numbers have certainly been compelling as quality private credit strategies have posted steady 10%+ returns (more than double what public bond alternatives have earned), while reporting lower day-to-day volatility than publicly-traded bonds. Double the earnings with less volatility? Yes, there is indeed a catch, and the downsides have kept us on the sidelines and instead targeting a broader public bond allocation in our core portfolios.

Recent events at one of the largest players, Blue Owl Capital, highlight the structural realities of this market. In early April, Blue Owl's two largest retail private credit funds faced massive redemption requests — roughly 22% of assets in their flagship fund and over 40% in their tech-focused fund. The firm responded by capping redemptions at the contractual 5% limit, honoring only a small fraction immediately and delaying the rest, potentially for years. This is not an isolated story; several other large private credit managers reported elevated withdrawal requests in the first quarter and have begun gating or limiting redemptions as well. The trigger appears to be growing investor concern around AI-driven disruption in software and SaaS companies (a sizable portion of many private credit portfolios), combined with the simple fact that these strategies are not marked to a daily market price like public bonds. Manager-marked values can make reported volatility look artificially low until investors actually try to exit. Add in quarterly (or less frequent) liquidity provisions, and you can see why we continue to view the space with caution.

I want to reiterate the point because it is very important: unlike publicly traded bonds whose prices are set by the market every day, private credit values are determined by the manager's own marks. Volatility looks artificially low because there is no daily trading to reveal the true swings.

Liquidity is almost always limited. Private credit funds only allow redemptions on a quarterly basis, which can become problematic precisely when investors need cash the most. In calmer times, these features felt like manageable trade-offs; today, with significant debt rollovers ahead and the potential for economic stress, they deserve extra scrutiny.

For now, we continue to largely hold off. Our job is to protect capital first, rather than chase yield and risk in the bond portion of your portfolio. I am interested to see if the risk/reward picture improves meaningfully, and we remain happy to discuss if you have any questions on the recent headlines and the firm’s current view on the asset class.

Thoughts on Market Valuations

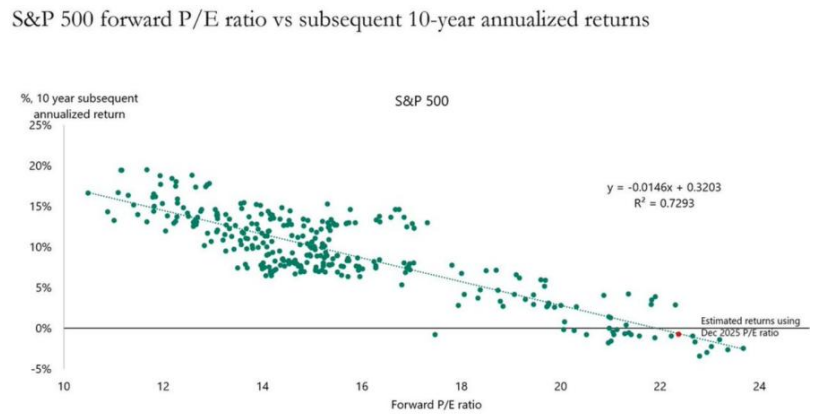

Another theme worth discussing in brief is valuation discipline. U.S. large-cap growth equities continue to trade at elevated multiples relative to historical standards and relative to many international and value-oriented markets. Depending on the measure you use, the S&P 500 is trading somewhere around 20 to 22 times forward earnings and 25 times trailing earnings. This is modestly above long-term averages and undeniably rich by traditional standards.

I used the illustration below in my January letter, but it is worth including again:

By historical standards, this graph is telling us we should expect muted returns from the S&P 500 over the next decade as earnings catch up with the companies’ current, modestly expensive valuations.

At the same time, it is important to acknowledge the narrative that investors are pricing in: an AI-driven productivity boom that could justify higher valuations if the technology delivers the kind of sustained earnings growth many expect. We have seen this playbook before where markets price in a brighter future, sometimes getting ahead of themselves, and sometimes getting it exactly right.

Our view is balanced: we are not abandoning the high-quality growth companies that have been excellent compounders, but we are also not comfortable concentrating the entire portfolio in large U.S. companies dominated by the tech sector.

This is why our global allocation and tilt toward value-oriented holdings remain central to the strategy. Developed international and emerging markets still trade at noticeable discounts to U.S. large caps on earnings, cash flows, and assets. Value stocks (companies priced more reasonably relative to their fundamentals) have historically delivered stronger long-term results when valuations become stretched elsewhere. Diversification across geographies, styles, and asset classes is not complication for complication's sake; it is the most reliable way we know to manage valuation risk over full market cycles.

The AI Revolution

No market letter in 2026 would be complete without addressing what I believe is the single most significant economic development of our lifetimes: the artificial intelligence boom. I want to share some thoughts, not as a tech analyst, but as someone watching how this is already reshaping industries, valuations, and eventually how we all live and work.

The headline name most people know is ChatGPT, which brought AI into the mainstream in late 2022 and made OpenAI a household name. What has been less appreciated, until recently, is how quickly a genuinely competitive landscape has emerged. Anthropic, the maker of Claude, has taken a meaningfully different path building tools aimed primarily at businesses and developers rather than retail consumers. Their focus on “agentic” AI (software that can actually complete multi-step tasks on your behalf, not just answer questions) is where much of the real productivity gain is starting to show up. Google, Microsoft, Meta, xAI, and several Chinese firms continue investing tens of billions of dollars. This is not a winner-take-all race, and the competition is healthy for consumers, businesses, and the broader economy.

Here is why this matters for your portfolio: The enthusiasm around AI is the single biggest reason U.S. large-cap growth stocks trade at the elevated multiples I discussed above. If AI delivers the productivity revolution its proponents expect (and I think it likely will, at least to some meaningful degree), then some portion of today's premium valuations will be justified in hindsight. If it disappoints on timing or magnitude, those same valuations will compress painfully. Nobody knows yet which it will be, and anyone who tells you they do is selling something.

Looking out over the next ten years, I believe we are likely to see changes to the economy and daily life on a scale commensurate with the Industrial Revolution. Entire categories of knowledge work will be transformed. Some industries will see profit margins expand dramatically; others will see their business models threatened. We are already seeing early signs of investor concern surrounding enterprise software (e.g., a driver of the private credit worries discussed earlier). The companies that benefit most a decade from now may not be today's obvious leaders.

Our response is not to chase the theme, nor to dismiss it. We continue to hold meaningful exposure to the technology leaders through our core equity allocations, but we balance that with value-oriented holdings and international diversification. A rising tide raises all boats.

One last thought on this: the greatest risk with a theme this powerful is not missing out, but instead it is overcommitting based on a story. The dot-com era taught us that being right about the technology and wrong about the valuation can still cost you a great deal of money. We intend to participate, but with discipline.

Closing Thoughts

Volatility is uncomfortable, but it is also where long-term returns are earned. Our strategy of maintaining liquidity, staying diversified across geographies and styles, and thoughtfully engaging with the AI theme rather than chasing it is exactly what we signed up to do together. Nothing about the current environment changes the plan.

As always, please reach out if you would like to discuss your portfolio, your financial plan, or anything else on your mind. I look forward to connecting with many of you in our upcoming meetings.

Thank you for reading. Please review our disclosures.

Subscribe to our Newsletter and Receive Important News & Updates.

Foundation Wealth & Tax Advisors is a Fee-Only, Fiduciary, Independent Financial Advisory Firm.

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.