July 2026 Letter

The fireworks have barely settled from Independence Day, and I find myself doing what I try to always do at the end of the quarter and mid-year mark: take a breath, look back at where we've been, and think hard about where we're headed. If you had asked me to bet in early April watching stocks sell off, that we'd close the first half of 2026 near record highs, I would not have taken that bet. And, yet, here we are.

Getting right to it: the second quarter was the strongest three months U.S. stocks have delivered since the pandemic recovery of 2020. The whiplash from Q1 to Q2 was a near-perfect illustration of why we invest the way we do, and it also planted a few warning flags underneath the surface that I want to walk you through. This is a mid-year check-in, so I'll keep it focused on what happened, what it means for your plan, and what I'm watching for the back half of the year. I also have to shout out America’s 250th birthday.

A Mid-Year Turnabout: The Best Quarter Since 2020

As I noted in my April letter, the S&P 500 finished the first quarter down roughly 4.3%, dragged lower by geopolitical fears, higher-than-average inflation, and worry over the wave of Treasury debt maturing this year. The mood was admittedly a bit sour.

I will say, the mood and optimism is still sour, but not if you look at the market in a vacuum. By the end of the second quarter, the S&P 500 has climbed back to roughly a 10% gain at the end of Q2, closing near 7,449 on June 30. That means the index gained something on the order of 15% in the quarter alone - its best quarter since 2020. The Nasdaq Composite did even better, finishing the first half up about 12.8% and closing near 26,214.

Here's the part I care about most, and it's a continuation of the story from April. The rally was not just a handful of mega-cap technology names doing the heavy lifting. Small-cap stocks (the smaller, more domestically-focused companies measured by the Russell 2000) came roaring back up over 20% year-to-date.

International developed and emerging markets held their ground as well, aided by a softening U.S. dollar (when the dollar weakens, the foreign holdings in your portfolio are worth more in dollar terms). International developed markets (measure by the MSCI World ex US index) ended June up roughly 9%, following a 32% return in 2025. International emerging markets (measured by the MSCI Emerging Markets index) finished the quarter up roughly 24% year-to-date after a remarkable 34% return in 2025.

Said simply: the pieces of your portfolio that felt like dead weight for stretches of the last few years like small companies, value equities, and international holdings, have been pulling their share of the load. This is exactly what a globally diversified portfolio is supposed to do. It is not designed to choose the winner in every quarter with every asset. It is designed so that when leadership rotates, as it inevitably does, something is always working and steady growth compounds over time in the market.

America at 250: Extraordinary, Not Invincible

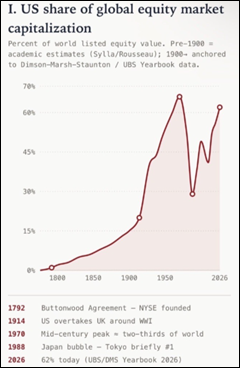

I say this to a lot of you when we speak, but valuation matters, and U.S. valuations are high by historical terms. A portfolio entirely driven by U.S. large cap equities is a riskier portfolio than you may think. It’s tough to want to invest abroad when so many incredible companies and technologies are U.S.-based, but it’s an important thing to do nonetheless. Today, over 60% of the world’s equity market capitalization is attributable to the U.S., and, if policymakers don’t muck it up, there is an argument that it can go much higher from here. Historically considering this mix, I find the image below fascinating and inviting some caution.

The higher you rise, the more room you have to fall. As the world order potentially reorganizes (e.g., the Europeans follow through on threats to break away from the U.S. technology stack), U.S. tech dominance, the largest driver of the U.S. market would be impaired. Similarly, if China wins the AI race and the world is built on Chinese hardware and models, that is bad news for U.S. tech valuations. The important message is to never be “all in” on one company or country.

None of my caution dims my view of this country. I have mixed feelings on the term “American Exceptionalism” as it has an aura of superiority to it. I do like to say America is extraordinary though. Reflecting on America’s 250th birthday, the country is extraordinary for a few reasons:

- America is the first large-scale democratic republic in human history. Sure, city states did it and sure, there were parliamentary monarchies, but we are the first to do it at scale.

- We have the oldest national constitution anywhere with separation of powers and checks and balances.

- I love the Bill of Rights. It goes so much further than the Magna Carta and really is the first time a nation wrote “the government cannot touch these” into law (and really meant it).

- We value success and ambitious hard work. In many other parts of the world and a minority of the U.S., success is equated with exploitation and ambition is looked upon with contempt. By and large here, striving is admired and success is celebrated. American innovation created the world’s largest economy since the turn of the 20th century - which, not coincidentally, gave the world the first controlled powered flight, and soon after the assembly line, then the skyscraper, then the transistor and personal computer. That spirit of invention has never stopped.

Property rights and extraordinary Americans power us through genius and grit. I celebrated all of this over the Fourth of July holiday weekend, and I will keep celebrating it while still owning investments in the rest of the world for you. Loving this country and diversifying beyond it are not in conflict.

A New Chairman and an Old Dilemma

For most of the past two years, the debate about the Federal Reserve has been when it would cut interest rates. This quarter, the conversation flipped, and it flipped under a new chairman. In May, the Senate confirmed Kevin Warsh as the 17th Chairman of the Federal Reserve by a 54–45 vote, the narrowest confirmation for a Fed chair in history, succeeding Jerome Powell. (In an unusual move, Powell is staying on the Fed’s Board of Governors as a regular member.) Chairman Warsh ran his first meeting in June, and I don’t think enough investors have absorbed what happened.

At its June 17 meeting, the Fed held its benchmark rate steady at 3.50%–3.75% for the fourth straight meeting in a unanimous 12–0 vote (Source: Federal Reserve). That part was expected. What caught markets' attention was the Fed's own "dot plot." This chart illustrates where each policymaker anonymously marks where they think rates are headed. The committee erased its earlier signal for a rate cut this year and pushed any reductions out into 2027 and 2028. The median projection now points to a year-end rate slightly above today's level, which means a rate hike is genuinely on the table (Source: Federal Reserve June SEP, CNBC). Nine officials penciled in a hike by year-end; only one saw a cut. The policy statement itself was slashed from 341 words to 130, dropped the prior language hinting that cuts were coming. Chairman Warsh, a longtime critic of the Fed’s forecasting rituals, declined to submit a dot of his own.

So, who is Kevin Warsh, and what should we expect from him? He served on the Fed’s Board of Governors from 2006 to 2011, sitting beside Chairman Ben Bernanke through the financial crisis, and he ultimately resigned rather than support a second round of large-scale quantitative easing. That history, plus his early rhetoric, gives the hawks plenty to point to. At his first press conference he said of inflation, “We’ve missed for five years and we’re going to fix that.” He has advocated a smaller Fed balance sheet, scrapped the committee’s forward guidance, and launched task forces to overhaul how the Fed measures inflation and communicates with the public. Markets read the June meeting as hawkish: the two-year Treasury yield jumped to its highest level in over a year that afternoon, and the dollar had its best day in nearly a year.

And yet the doves have their own reading of the very same man. He was appointed by a president who has been loud and public about wanting lower interest rates. Before his nomination, Warsh argued that AI-driven productivity gains would push inflation down and give the Fed room to cut, and he has characterized tariffs as one-time price bumps rather than lasting inflation. He has also suggested an interesting middle path: cutting short-term interest rates while simultaneously shrinking the Fed’s balance sheet - essentially easing with one hand while tightening with the other. Said simply, Chairman Warsh’s rhetoric offers both hawks and doves something to hold onto, and I suspect that is partly by design. My plan is to watch what he does, not what he says. Time will tell which Warsh shows up.

While everyone stares at interest rates, I want to draw your attention to a quieter number I follow closely - the money supply or “M2.” M2 is the broad measure of dollars in the system including cash, checking and savings accounts, CDs, and money market funds. After actually shrinking in 2022 and 2023 (a historically rare event), M2 is growing again at roughly 4–5% year-over-year and now sits at an all-time high of about $22.8 trillion (Source: Federal Reserve, FRED). Said a different way: even while the Fed holds interest rates steady, the number of dollars in the system keeps climbing.

Why does that matter? When the money supply grows faster than the economy produces goods and services, each dollar buys a little less over time. Steady rates get the headlines, but a growing money supply does quiet work in the background — supporting asset prices while keeping upward pressure on the cost of living. It is one more reason I believe the inflation of recent years is not fully behind us.

It is my strong opinion that prices follow the money supply. As long as money supply growth outpaces true economic growth, you should expect purchasing power to decline.

Beneath the Rally: Valuations and the Melt-Up Risk

We have a market at record highs, and a Fed warning about inflation with yields rising. How do I hold both of those in my head at once? Carefully.

The engine under this rally is real: corporate earnings. As the second quarter closed, analysts expected S&P 500 companies to report year-over-year earnings growth north of 23% (Source: FactSet). That is not a fragile, story-driven melt-up on nothing - profits are genuinely expanding, margins are widening, and the AI investment cycle has started showing up in actual results, particularly across the semiconductor complex, which had an incredible quarter. This is the strongest argument for the bulls, and I want to give it its full due: if earnings keep compounding at anything close to this pace, today's valuations look a good deal more reasonable in hindsight.

And, now the other side, because it wouldn't be one of my letters without it. Even with strong earnings, U.S. large-cap stocks are not cheap. After a 15% quarter, the S&P 500 again trades at a premium to its own history and a wide premium to international and value-oriented markets. When you buy at rich valuations, history is fairly consistent that you should expect below-average returns soon after. This is not because the companies are bad, but because you've paid up for them. The greatest danger with a theme as powerful as AI is not missing out; it's overcommitting to a story and paying any price to own it. You can be exactly right about a technology and still lose money badly if you overpay for it.

Our answer is the same as it has been, and I make no apology for its consistency: we participate in the growth leaders through our core equity holdings, but we deliberately balance them with value stocks, smaller companies, and international exposure that trade at meaningful discounts. We are not abandoning great compounders, and we are not concentrating your life savings in a dozen expensive names because a narrative is exciting. The last two quarters, where the "boring" parts of your portfolio did real work, are the proof.

Closing Thoughts

The first half of 2026 has been another reminder that markets rarely move in straight lines. We started the year with declines, only to find ourselves discussing record highs a few months later. That kind of reversal is exactly why I resist making dramatic portfolio changes in and out of the market and instead focus on global diversification and managing liquidity. As we head into the second half of the year, I remain optimistic but disciplined. Strong corporate earnings, continued innovation, and a resilient economy give us reasons for confidence, while elevated valuations, persistent inflation risks, and geopolitical uncertainty remind us to stay diversified and focused.

If you have not heard from us yet regarding your summer meeting, please know you will soon. Thank you, as always, for the trust you place in us. Looking forward to catching up soon.

Thank you for reading. Please review our disclosures.

Subscribe to our Newsletter and Receive Important News & Updates.

Foundation Wealth & Tax Advisors is a Fee-Only, Fiduciary, Independent Financial Advisory Firm.

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.