SpaceX, Musk, and the Math of a $1.75 Trillion IPO

SpaceX filed its S-1 last Wednesday, aiming to raise $75 billion at a $1.75 trillion valuation. If it prices there, it would be the largest IPO in history - nearly double Saudi Aramco. The listing is expected mid-June.

A deal this size seems pulls everyone in. Headlines, group chats with my tech friends, the inevitable client questions about whether to put money in. So I want to share how I look at it, what the filing actually says, and where I currently land (which, fair warning, is a place that may sound boring).

My job is to protect client capital first, and to participate in growth at sensible prices second. I cannot know where the share price goes after IPO, and I am not going to pretend otherwise. There is a difference between understanding a company and having an opinion on its IPO price. I have the first. I do not have the second, and I am not in the business of speculating with money my clients need.

Getting to the S-1 disclosure…SpaceX runs three businesses, and they look very different from each other on the financials.

- Starlink Satellite Internet is the cash cow. $11.4 billion in revenue last year, growing 50%, with $4.4 billion in operating profit. Roughly 10 million subscribers today; some analysts see a path to hundreds of millions if it becomes a dominant global internet provider.

- Space and Reusable Rockets did about $4 billion in revenue with 17% growth, but lost roughly $650 million at the operating line.

- Artificial Intelligence did $3.2 billion in revenue and doubled, but lost $6.2 billion.

The losses are largely “capex” building out AI compute and reusable-rocket capacity. Whether those are good or bad losses depends entirely on what they earn going forward.

One newer business line worth flagging: SpaceX is starting to rent excess compute capacity to outside AI companies, including Anthropic, at a reported run rate of $1.25 billion per month beginning this spring. If sustainable, that meaningfully changes the AI segment’s trajectory.

The Case for Caution

The valuation math. At $1.75 trillion, SpaceX would trade at roughly 94 times revenue and an infinite multiple on GAAP earnings. For context, Apple trades at around 9 times revenue and Microsoft at 13—two of the most profitable companies in history. An asset’s price is a forecast of its future. The higher the multiple, the more perfect the execution required. Paying this price is not a bet on success; it is a bet on flawless performance across rocket launches, satellite internet, direct-to-cell service, space-based data centers, and a successful Mars program over the next decade, with no major setbacks.

Non-voting reality for public shareholders. The S-1 discloses super-voting Class B shares that give Musk roughly 85% of the voting power while holding about 42% of the equity. Public shareholders will own most of the company and control almost none of it. That is not unusual in modern tech IPOs, but it is worth knowing what you are buying.

Index inclusion is uncertain. A fun one for the nerds among us. SpaceX would debut large enough to rank among the biggest U.S. companies, but most major indices, including the S&P 500, require positive GAAP net income in the most recent quarter and over the trailing four quarters. With a $4.94 billion GAAP net loss in 2025, SpaceX would not qualify on day one, no matter how big the market cap. Index providers are literally working out how to handle a company this size that is not yet profitable on paper. For investors expecting passive flows to automatically support the price, that is a misread of the rules.

History rhymes. Being right about the technology and wrong about the valuation can still be costly. Cisco was correct about the importance of the internet, and investors who bought at the 2000 peak are still waiting to break even in real terms 25 years later. Recent IPOs make the same point in both directions. Reddit, Arm Holdings, and CAVA delivered strong returns from reasonable offering prices. Instacart and especially Rivian—which debuted at an $86 billion valuation and has burned capital since—show what happens when the price embeds too much of the future.

The Case for the Bulls

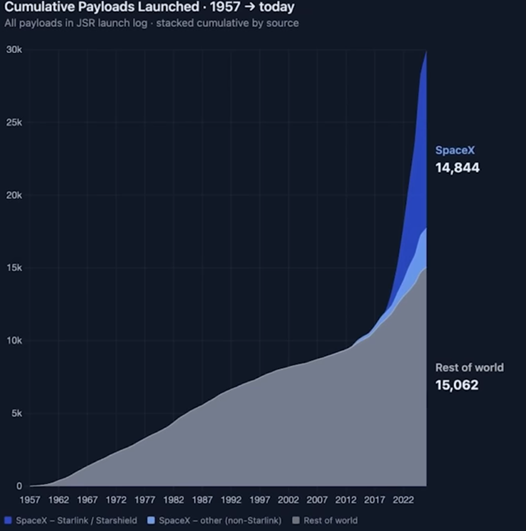

Operational efficiency that is genuinely hard to replicate. The first SpaceX data center took 120 days to build. The second took 91. The third took 66. They are building data center capacity dramatically faster and cheaper than competitors. On the rocket side, SpaceX’s cumulative payload to orbit since 2012 is on pace to exceed every other launch provider in the world combined. Efficiency at this scale tends to compound.

The Cursor acquisition. xAI was meaningfully behind Google, OpenAI, and Anthropic on AI models and tooling. Rather than spend years catching up, they look to be buying Cursor, one of the fastest-growing developer-AI products on the market. It may be a very smart use of capital. Buying revenue, talent, and product-market fit at once is faster than building any one of them from scratch. It does not solve the model gap entirely, but it shortens the path considerably.

Growth bends the math. If you believe revenue doubles by 2026/2027 and roughly doubles again by 2029 (which is what some analysts project) then today’s 94x revenue is closer to 20x revenue on out-year numbers. That is still expensive, but it is in a more recognizable neighborhood. The bull case is not that the valuation is reasonable today; it is that growth catches the valuation.

Where I Come Out

Two things can be true at the same time. SpaceX is a remarkable company building real, durable, important businesses. And paying $1.75 trillion for it requires the future to arrive on schedule, with very little going wrong along the way.

Said simply: our role is to pay rational prices for durable cash flows and to avoid the mistakes that become obvious only in hindsight. At $1.75 to $2 trillion, SpaceX is pricing in a future that may arrive or may not arrive. I am content to watch from the sidelines, or to gain exposure eventually through index inclusion and the ETFs we already use.

If you’d like to talk through this—you know how to reach me.

Thank you for reading. Please review our disclosures.

Subscribe to our Newsletter and Receive Important News & Updates.

Foundation Wealth & Tax Advisors is a Fee-Only, Fiduciary, Independent Financial Advisory Firm.

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.